Ledgerly

Categories

Fintech

Mobile App

Duration

2025-2026

Role

Product designer

Client

Side-Project

Overview

Helping Businesses Track Money, Send Invoices, and Access Credit

Designing a mobile-first fintech platform that helps small & medium businesses track money, send invoices, and access credit

While working on various fintech projects, I noticed a pattern: small business owners in Nigeria constantly struggled with cashflow visibility and access to working capital.

I started Ledgerly as a side project to explore: What if we could embed credit directly into the payment flow, turning invoices into instant working capital?

The Problem

Spreadsheets, WhatsApp, and Loan Sharks: Understanding How SMBs Actually Survive

Even as a side-project, I still had to put on my "UX research hat" to figure out what existing issues affected these SMBs. After speaking to some small business owners and close friends, I identified 3 critical issues:

Invisible cash flow: Most of them were used to tracking money in spreadsheets or paper notebooks. Most can't answer "How much did I make last month?" without spending hours reconstructing records.

Unprofessional payment collection: Sending bank details via WhatsApp feels informal and leads to errors, delayed payments, and lost revenue.

Credit access gap: Banks won't lend to informal businesses. When a large order comes in requiring upfront inventory purchases, business owners resort to high-interest "loan sharks" (20-30% monthly interest) or simply reject the opportunity.

From a product & business perspective, having an embedded finance opportunity was useful but challenging:

Lending to some of these SMBs without traditional credit histories requires alternative underwriting models.

Understanding the issues from the user and product perspective, I decided to craft a north-star problem statement that guided my design thinking from here on:

How do we design a product where each feature reinforces the others—where invoicing generates data for credit decisions, and credit access incentivizes more invoicing—creating a flywheel effect?

Opportunity

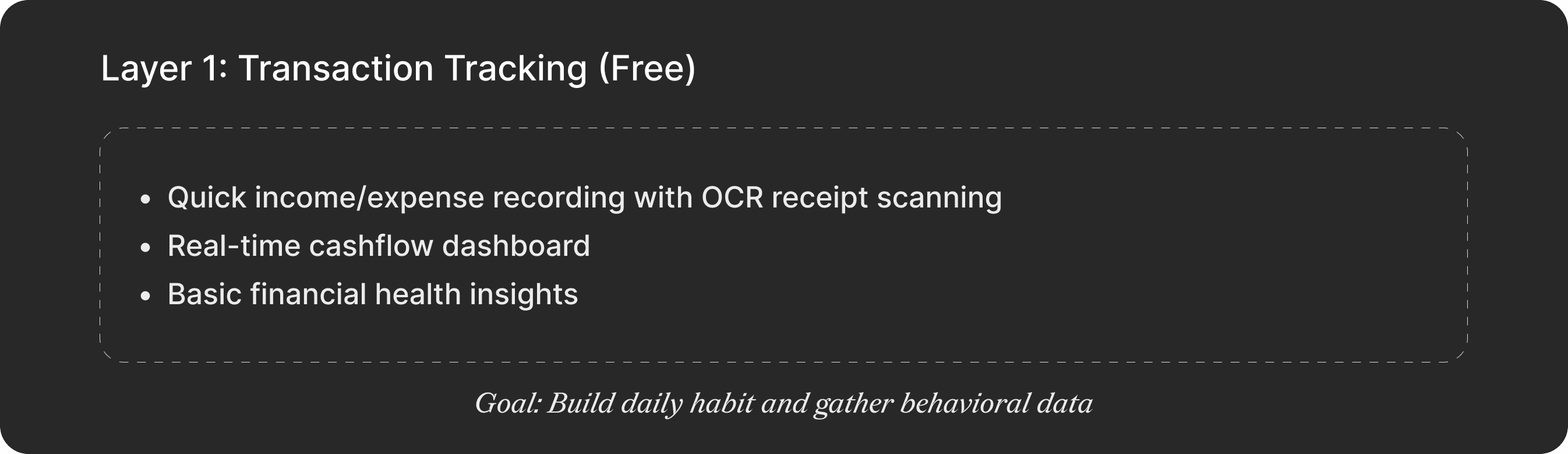

Progressive Value Delivery

Rather than building a feature-rich financial platform, I designed an interconnected product where each capability strengthens the other.

I structured the product as a value ladder where users naturally progress through increasingly valuable (and monetizable) features:

Solution

Key Design Decisions

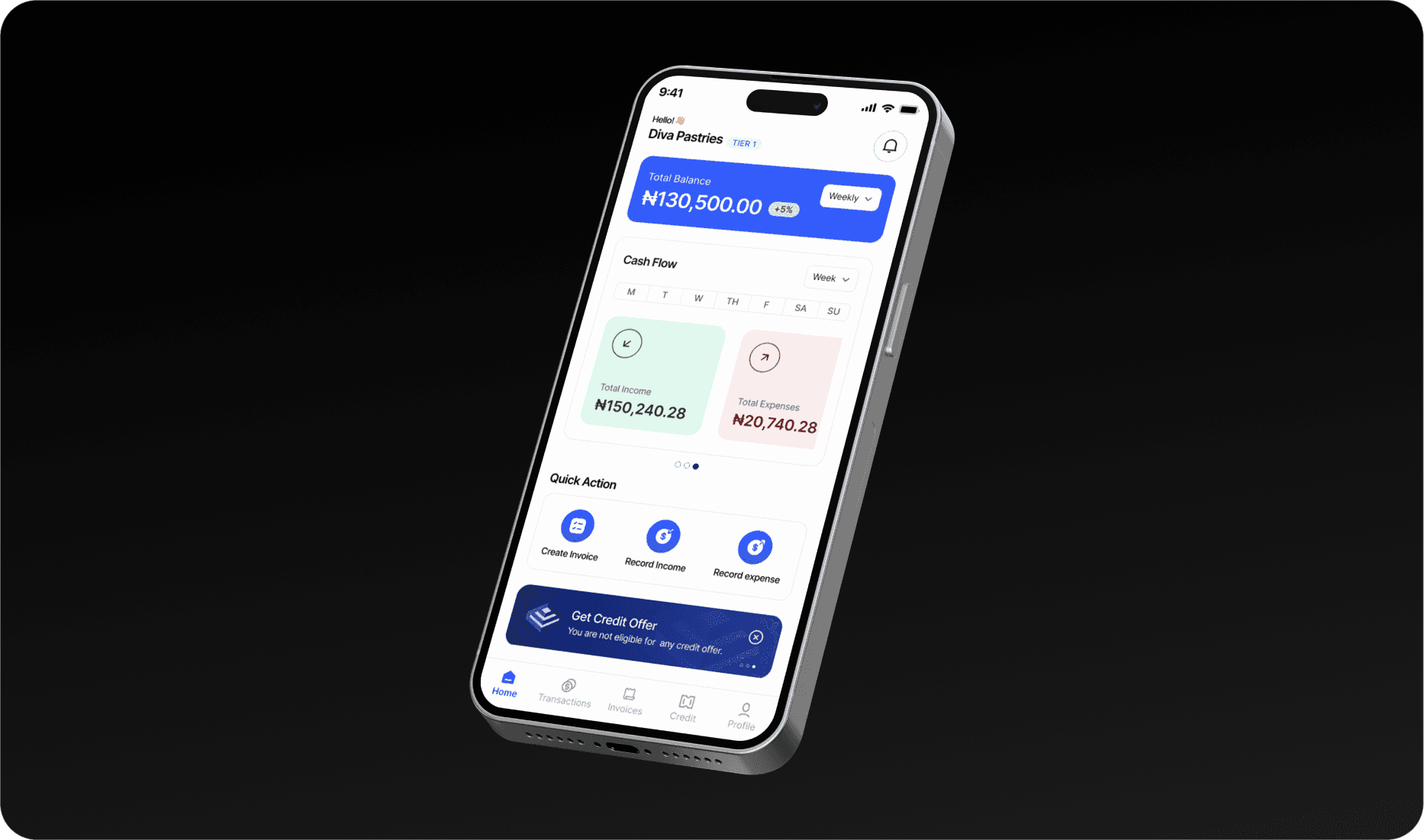

Improving how users create invoices, recover funds and record expenses.

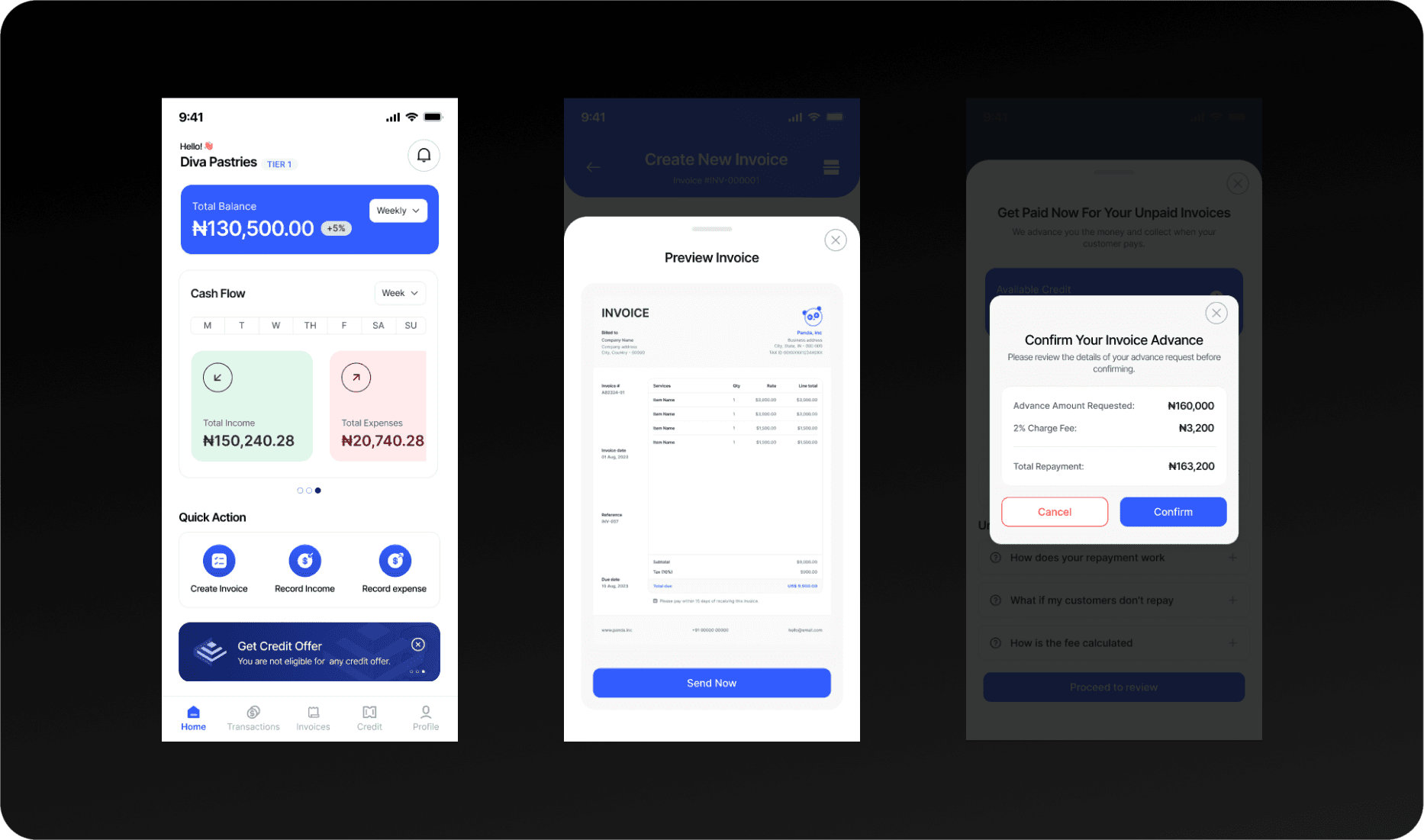

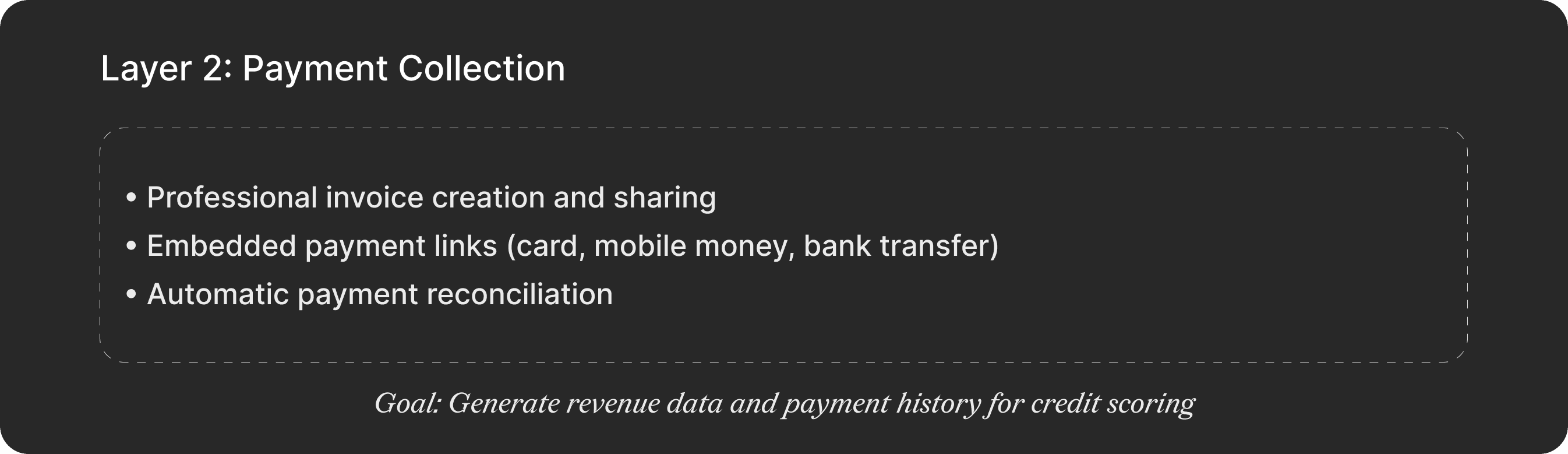

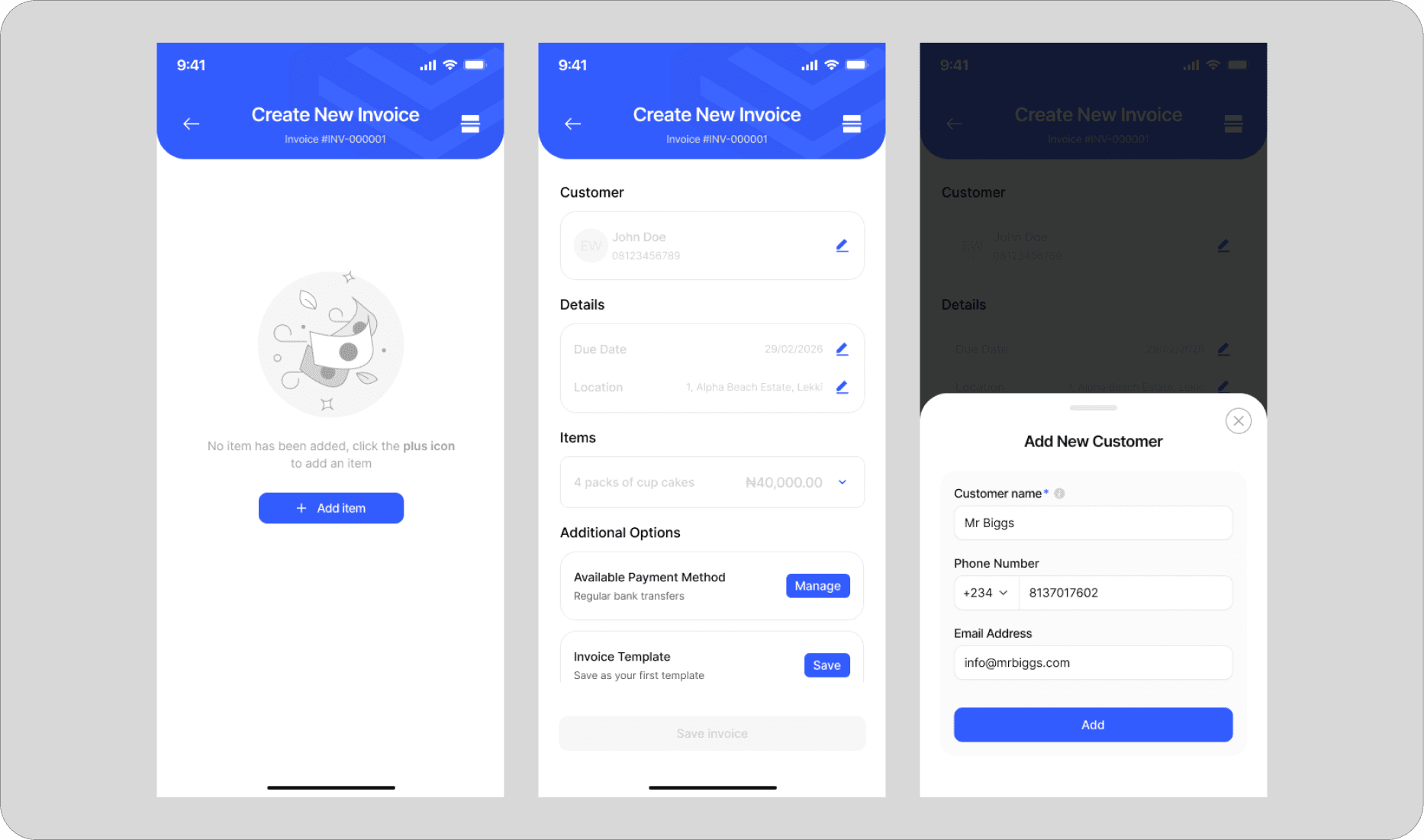

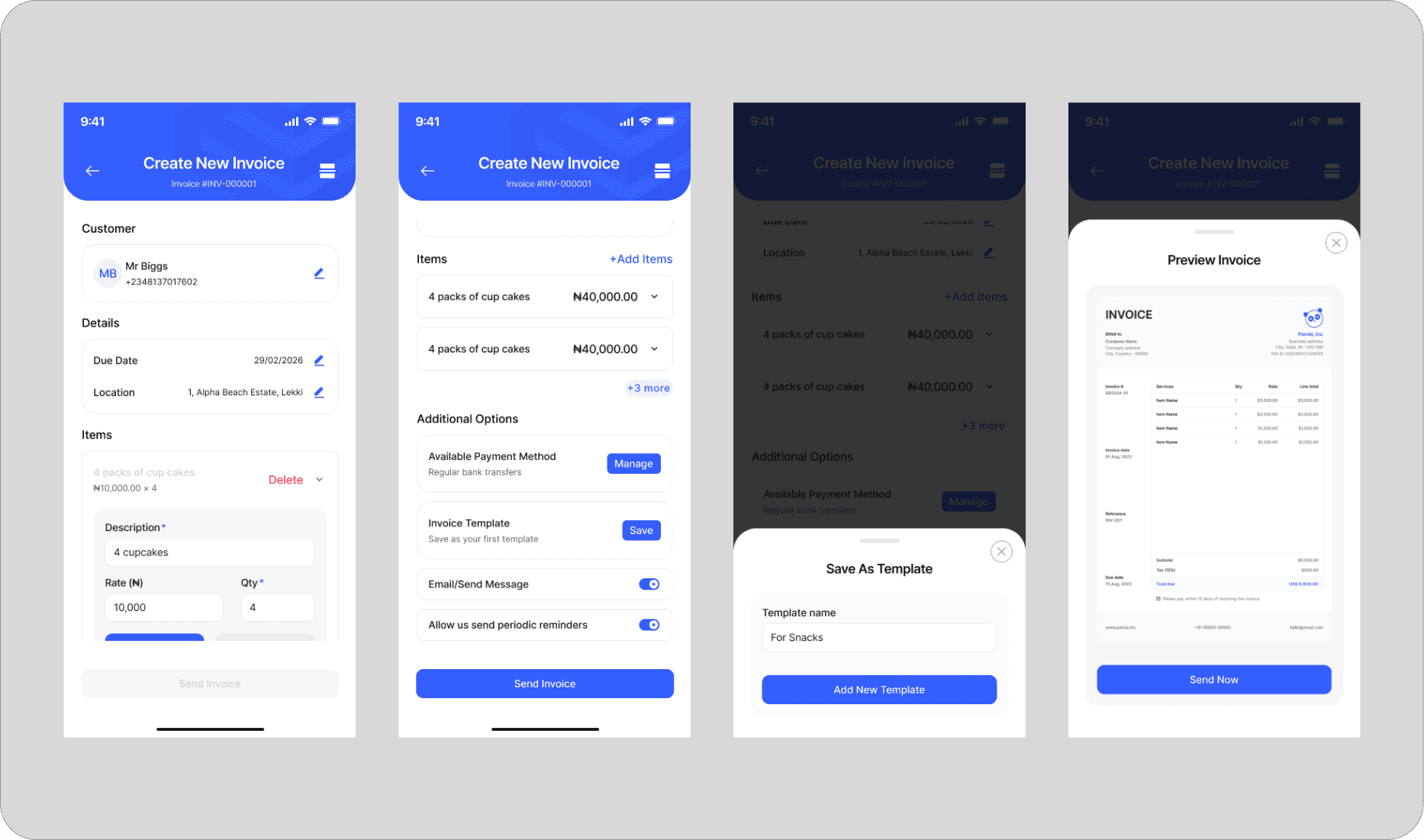

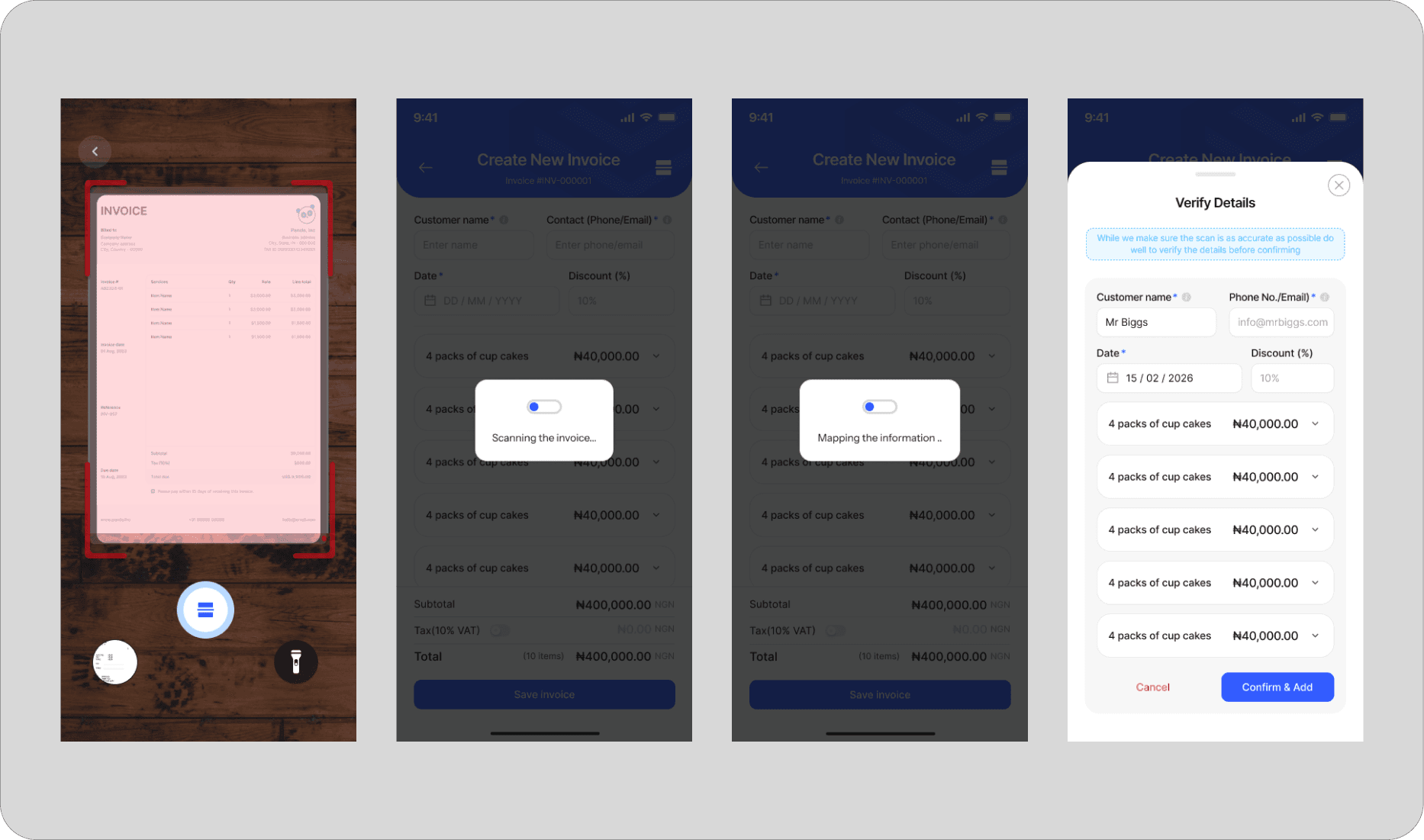

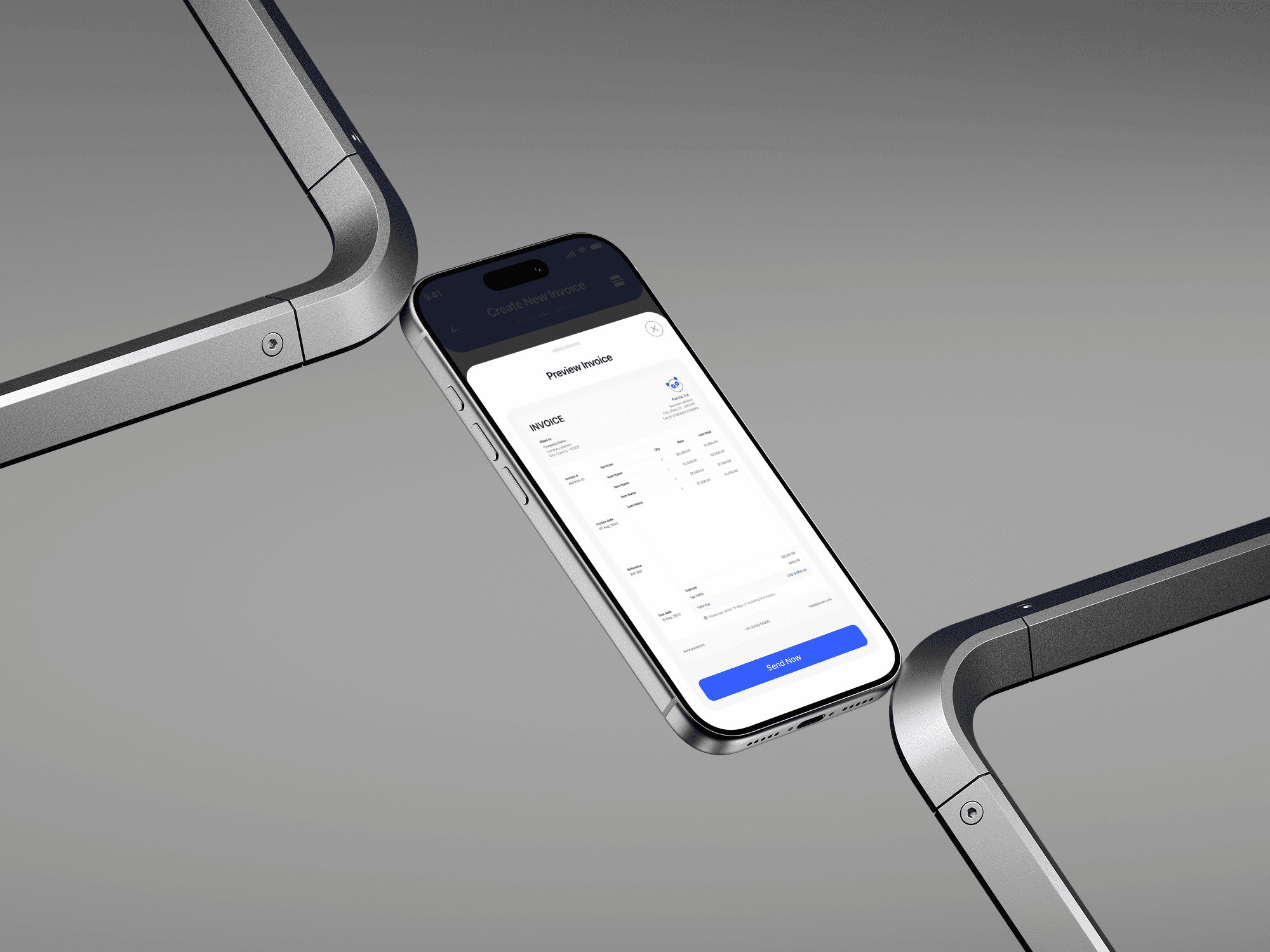

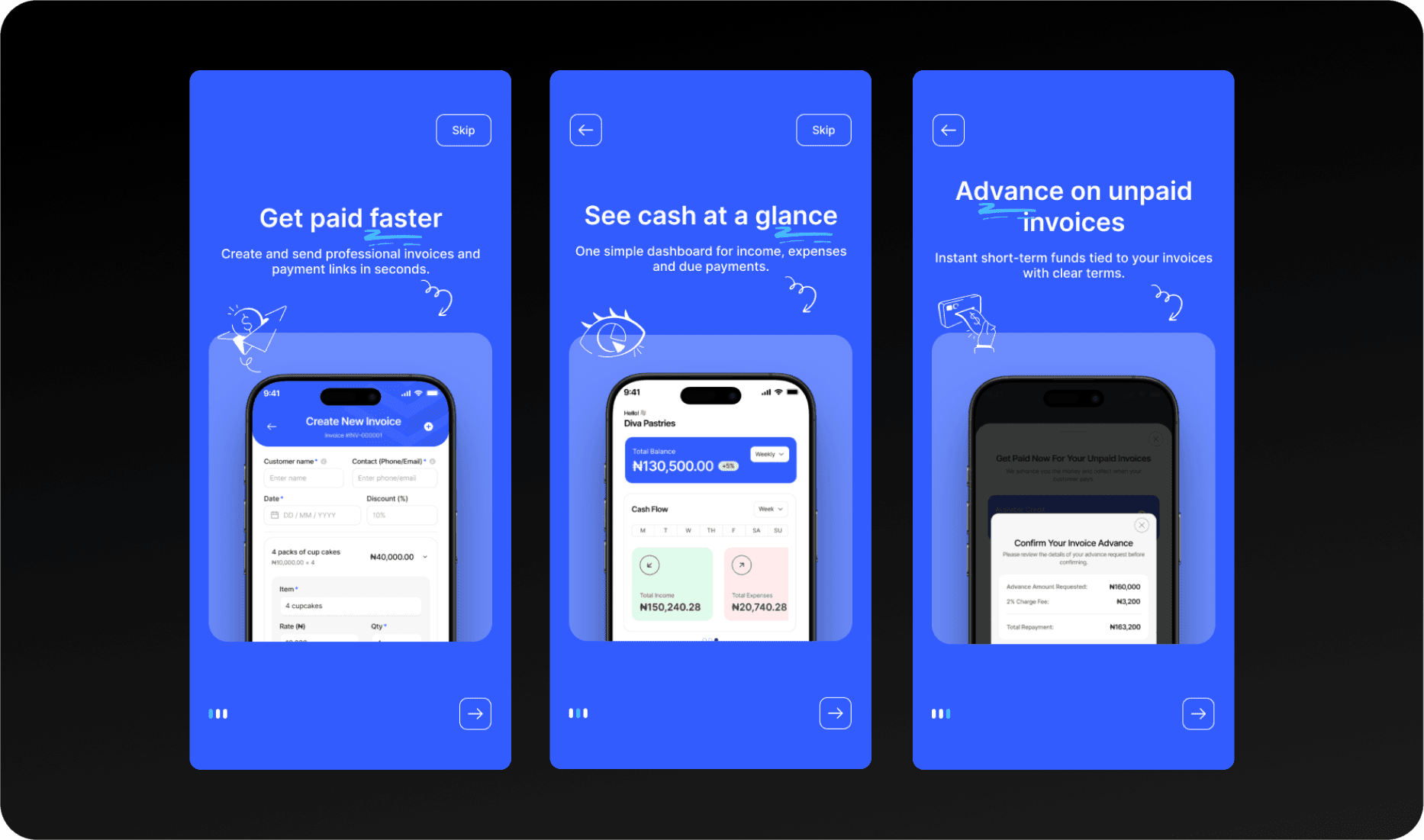

Users can create invoice templates to reduce the time spent on invoice creation. Invoices are sent to customers, who can pay automatically via an embedded payment link, and the user is notified when payment has been made.

To improve fund collection, the system periodically sends payment reminders to customers and enhances business fund collection.

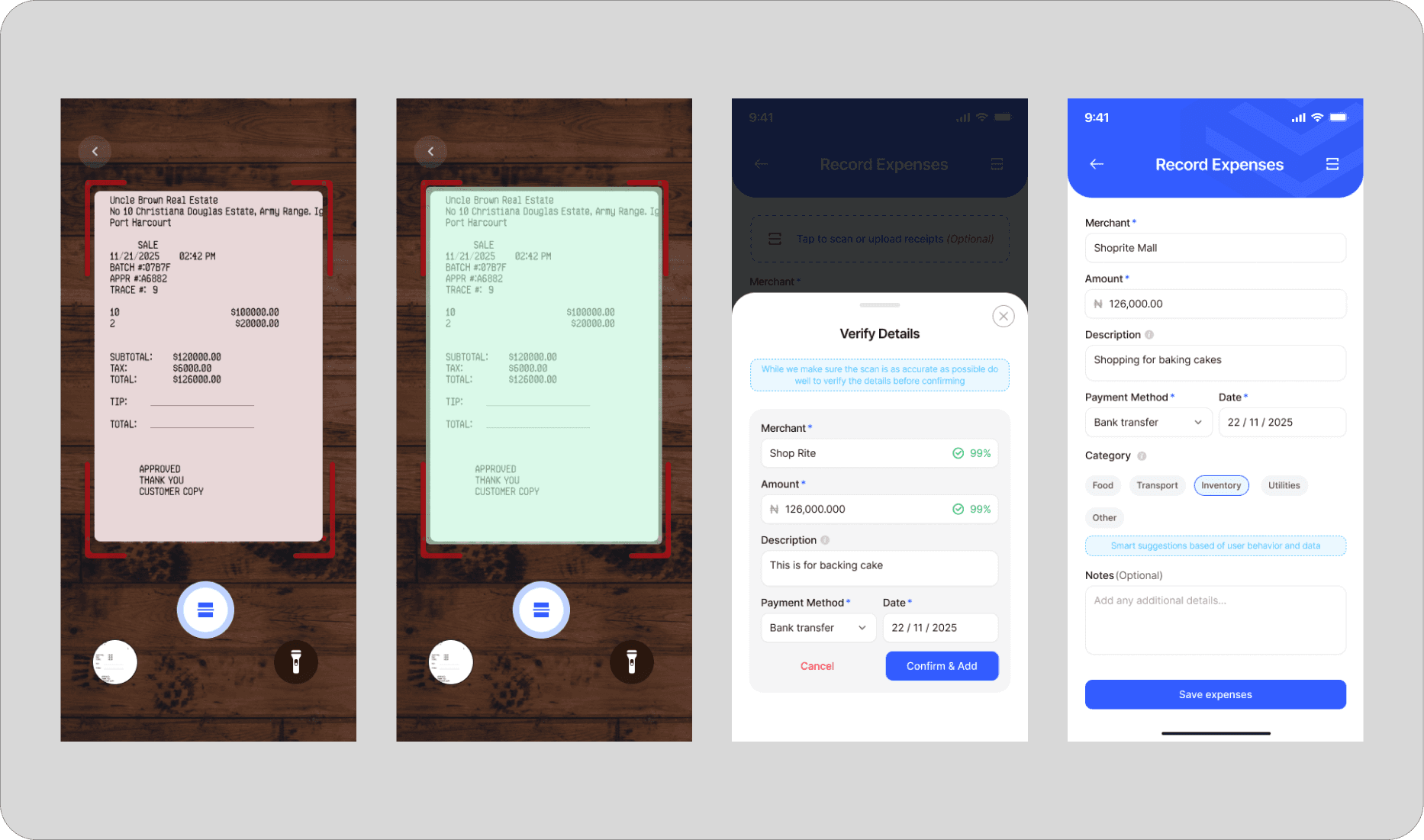

Quick income/expense recording with OCR receipt scanning

Design for the 30-second use case

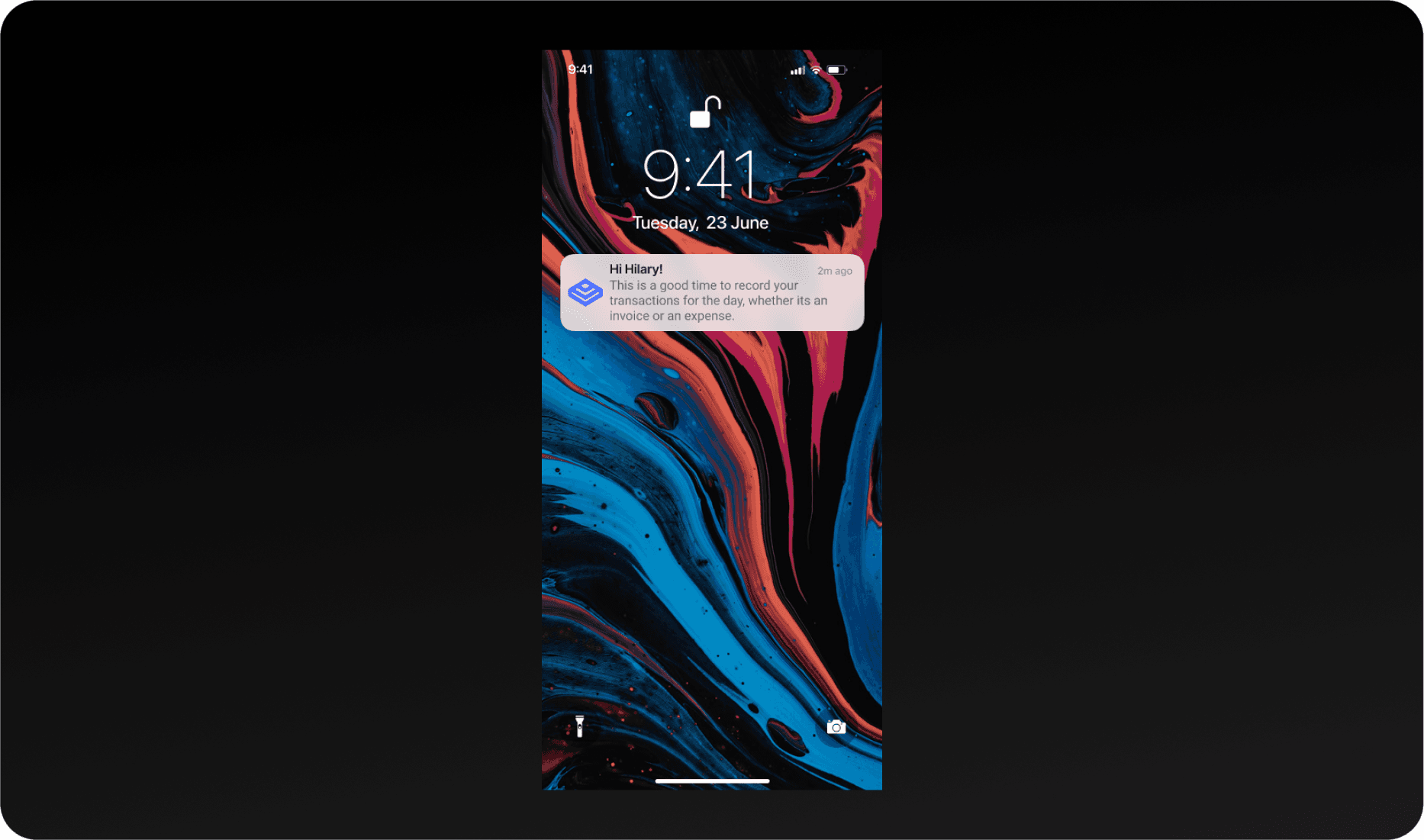

SMB owners rarely have 10 minutes to "do their books." The product had to work in stolen moments—between customers, during a commute, before bed. So, having a push notification that reminds users to record their daily financial activities would help users stay disciplined with their bookkeeping.

Intelligent defaults & smart suggestions over configuration

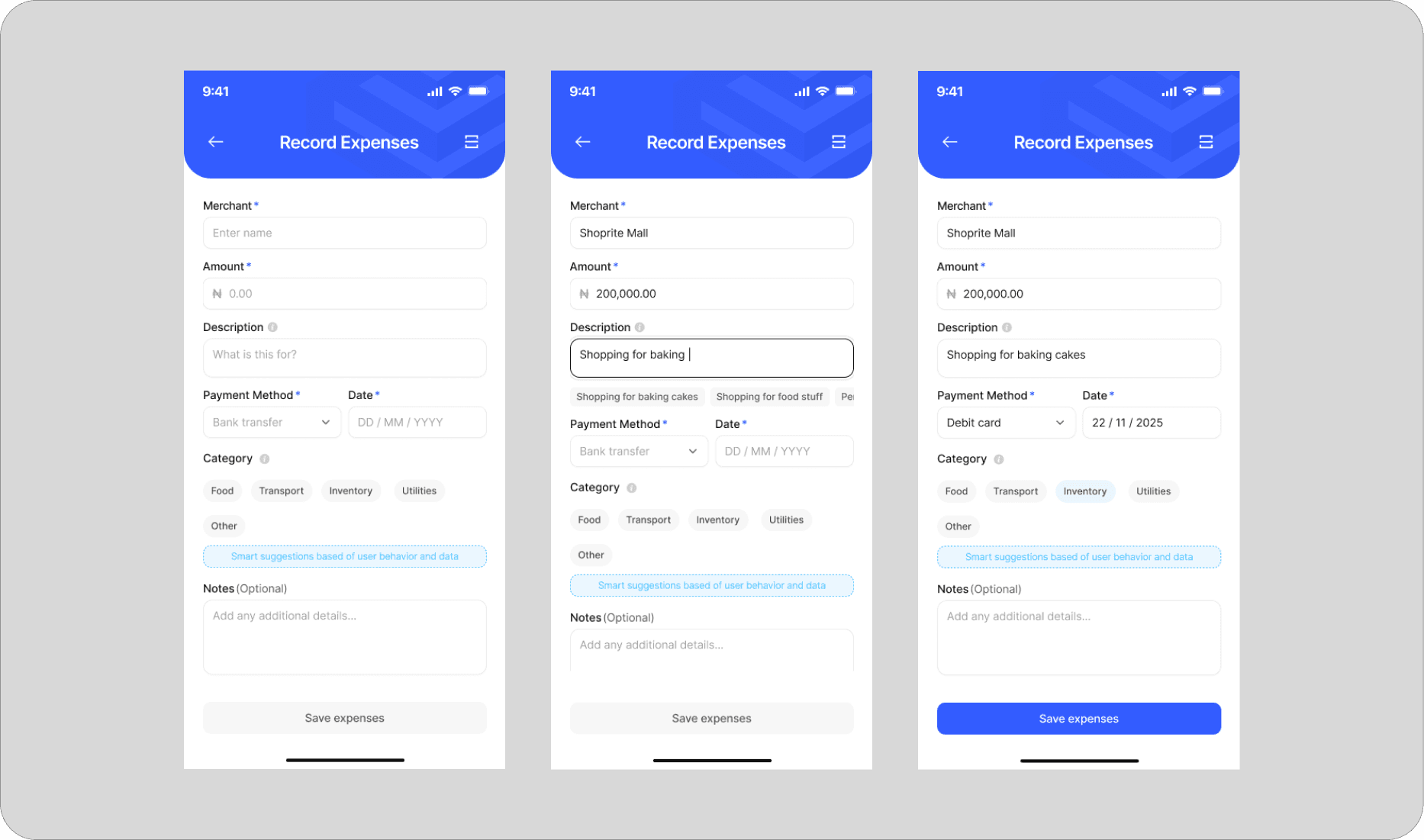

Based on user data and interaction with the app, the system auto-suggests possible descriptions of the user's expenses, and categories are based on past activities of the user. For instance, instead of asking users to categorise expenses manually, the system learns patterns and behaviour of the user, thereby personalising the experience of the user.

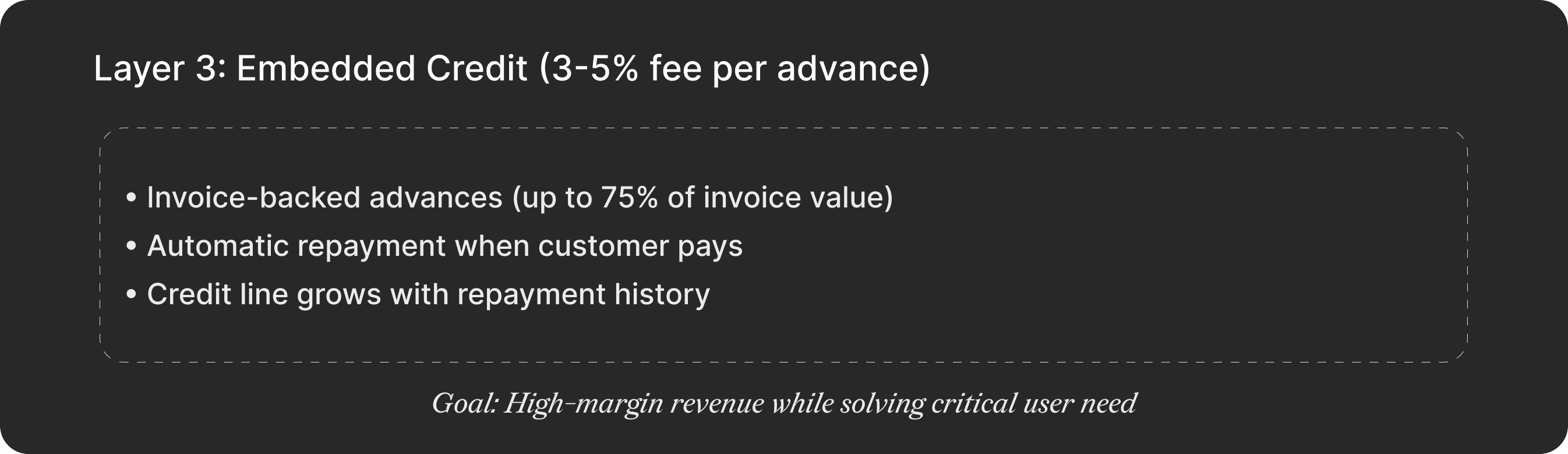

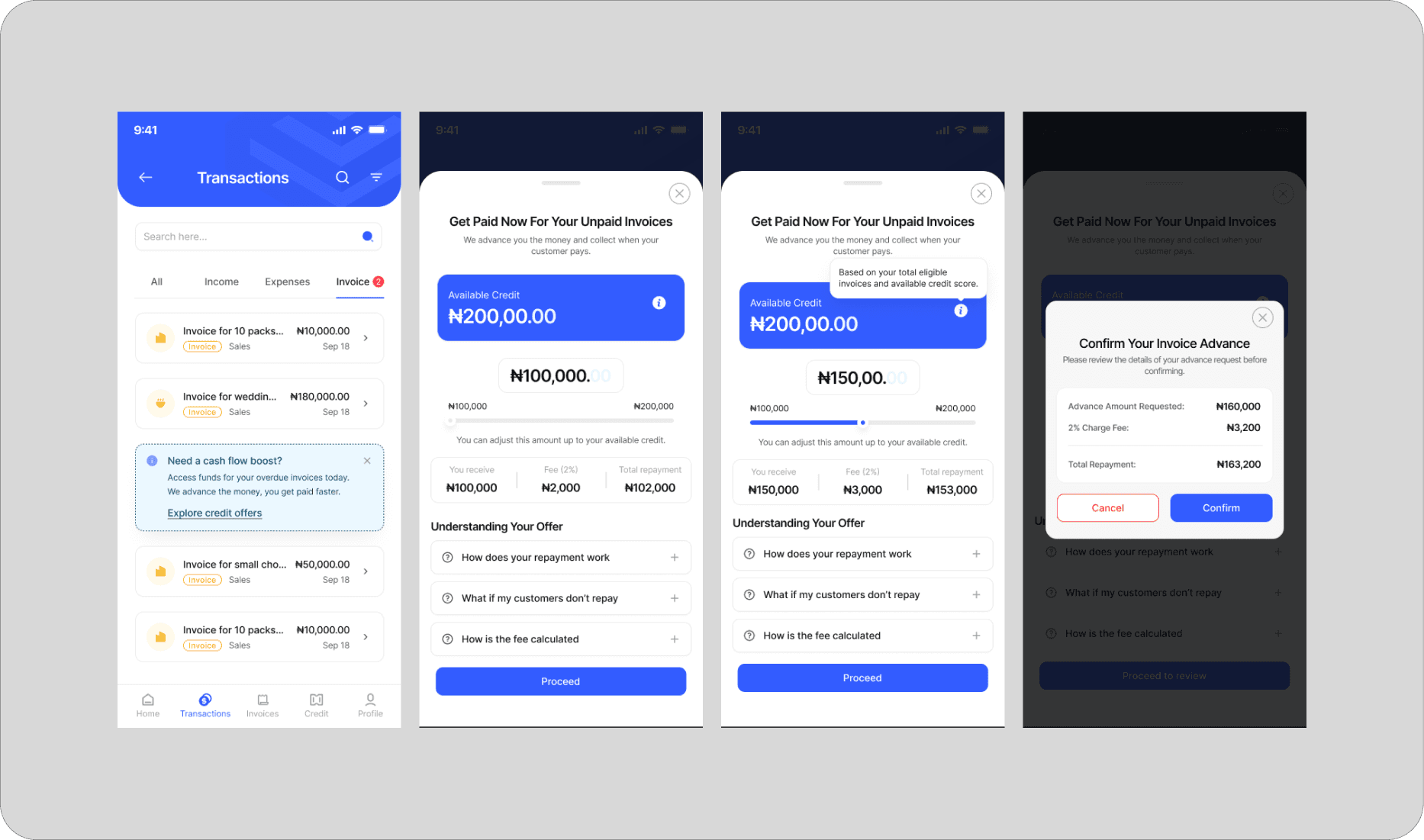

Contextual credit offers, not loan applications

Rather than making users "apply for a loan," credit appears contextually when they have unpaid invoices: "Customer hasn't paid yet? Get your money now—we'll collect when they pay." This reframing would change the mental model from "taking debt" to "accelerating my own money and helping my business to grow." This would reduce psychological resistance to credit.

Reducing the complexity of credit accessibility

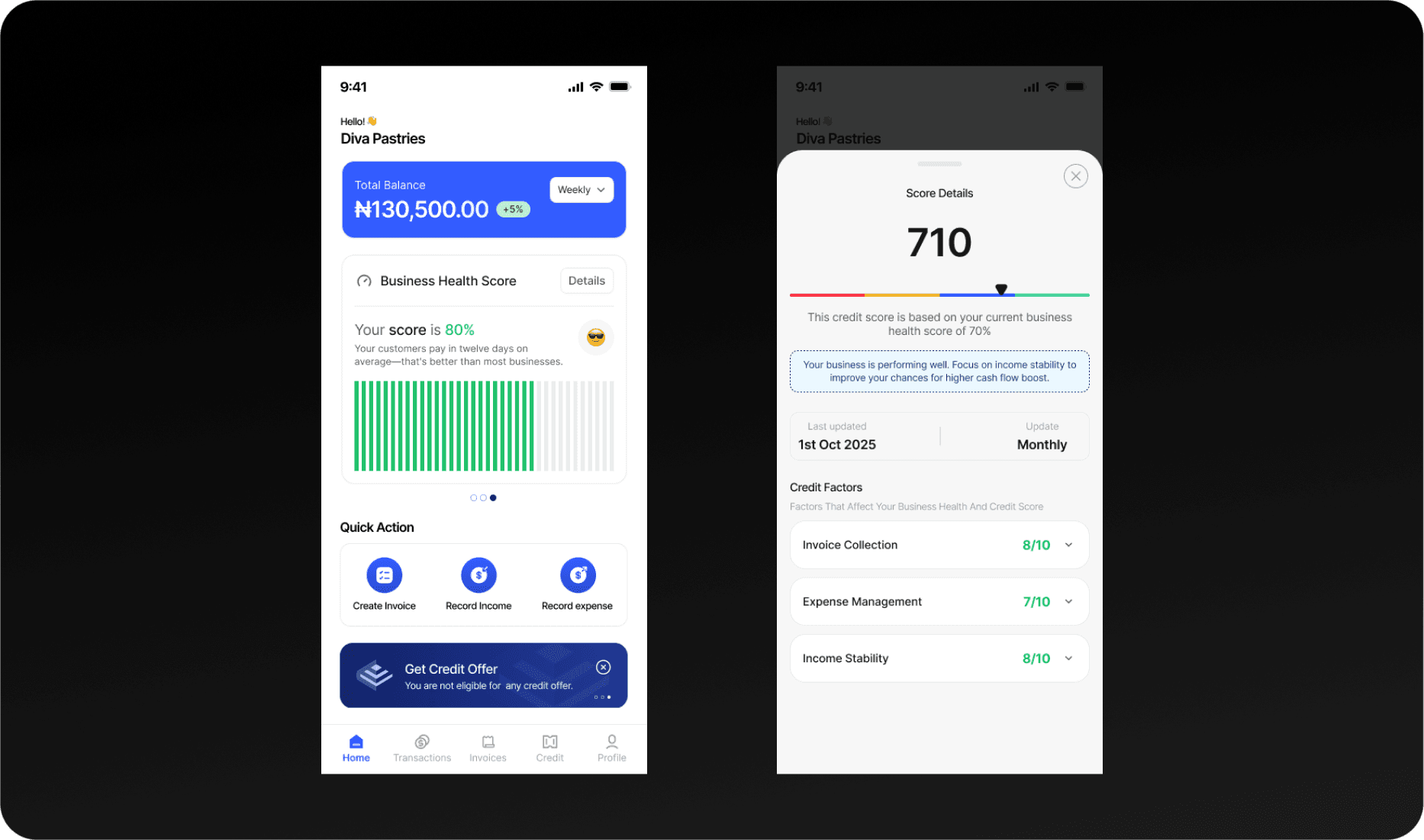

One thing I discovered is that SMBs are quite sceptical when it comes to getting credit for their businesses, as they see it as a debt trap in the hands of regular loan sharks. To reduce any form of uncertainty, I created a feature that shows users how these credits are calculated and how they can be accessed.

Conclusion

Biggest Learning: Design for Behaviour Change, Not Just Workflows

Even as a side project, the challenge wasn't designing screens; it was designing a system that convinced business owners who've managed money informally for years that tracking digitally was worth the effort. Every micro-interaction needed to provide immediate feedback that reinforced "this is making my business better."

Each feature isn't valuable in isolation. Value compounds when features feed into each other. Transaction tracking generates data → Invoicing creates credit opportunities → Credit usage drives more invoicing. Design the flywheel, not the features.

What I'd Change, if I had time and the resources:

1. Earlier testing of the payment flow

I designed the invoice payment experience based on assumptions about what would work. Reviewing the product with a couple of users, I discovered that users were confused by the split-settlement model (where payments partially repay credit). Should have prototyped this interaction much earlier, it's the core value prop.

2. More focus on "why", not just "how"

Initial designs showed users what to do ("Create an invoice") but not why it mattered to their business. Adding contextual education ("Professional invoices get paid 5 days faster on average") improved feature adoption. Should have led with value, not functionality.

3. Accounting for intermittent connectivity earlier

Halfway through the project, I realised many users would have unreliable mobile data. Redesigning for offline-first was painful. Should have made "works on 3G/intermittent connection" a core constraint from day one, not an afterthought.

Ledgerly

Categories

Fintech

Mobile App

Duration

2025-2026

Role

Product designer

Client

Side-Project

Overview

Helping Businesses Track Money, Send Invoices, and Access Credit

Designing a mobile-first fintech platform that helps small & medium businesses track money, send invoices, and access credit

While working on various fintech projects, I noticed a pattern: small business owners in Nigeria constantly struggled with cashflow visibility and access to working capital.

I started Ledgerly as a side project to explore: What if we could embed credit directly into the payment flow, turning invoices into instant working capital?

The Problem

Spreadsheets, WhatsApp, and Loan Sharks: Understanding How SMBs Actually Survive

Even as a side-project, I still had to put on my "UX research hat" to figure out what existing issues affected these SMBs. After speaking to some small business owners and close friends, I identified 3 critical issues:

Invisible cash flow: Most of them were used to tracking money in spreadsheets or paper notebooks. Most can't answer "How much did I make last month?" without spending hours reconstructing records.

Unprofessional payment collection: Sending bank details via WhatsApp feels informal and leads to errors, delayed payments, and lost revenue.

Credit access gap: Banks won't lend to informal businesses. When a large order comes in requiring upfront inventory purchases, business owners resort to high-interest "loan sharks" (20-30% monthly interest) or simply reject the opportunity.

From a product & business perspective, having an embedded finance opportunity was useful but challenging:

Lending to some of these SMBs without traditional credit histories requires alternative underwriting models.

Understanding the issues from the user and product perspective, I decided to craft a north-star problem statement that guided my design thinking from here on:

How do we design a product where each feature reinforces the others—where invoicing generates data for credit decisions, and credit access incentivizes more invoicing—creating a flywheel effect?

Opportunity

Progressive Value Delivery

Rather than building a feature-rich financial platform, I designed an interconnected product where each capability strengthens the other.

I structured the product as a value ladder where users naturally progress through increasingly valuable (and monetizable) features:

Solution

Key Design Decisions

Improving how users create invoices, recover funds and record expenses.

Users can create invoice templates to reduce the time spent on invoice creation. Invoices are sent to customers, who can pay automatically via an embedded payment link, and the user is notified when payment has been made.

To improve fund collection, the system periodically sends payment reminders to customers and enhances business fund collection.

Quick income/expense recording with OCR receipt scanning

Design for the 30-second use case

SMB owners rarely have 10 minutes to "do their books." The product had to work in stolen moments—between customers, during a commute, before bed. So, having a push notification that reminds users to record their daily financial activities would help users stay disciplined with their bookkeeping.

Intelligent defaults & smart suggestions over configuration

Based on user data and interaction with the app, the system auto-suggests possible descriptions of the user's expenses, and categories are based on past activities of the user. For instance, instead of asking users to categorise expenses manually, the system learns patterns and behaviour of the user, thereby personalising the experience of the user.

Contextual credit offers, not loan applications

Rather than making users "apply for a loan," credit appears contextually when they have unpaid invoices: "Customer hasn't paid yet? Get your money now—we'll collect when they pay." This reframing would change the mental model from "taking debt" to "accelerating my own money and helping my business to grow." This would reduce psychological resistance to credit.

Reducing the complexity of credit accessibility

One thing I discovered is that SMBs are quite sceptical when it comes to getting credit for their businesses, as they see it as a debt trap in the hands of regular loan sharks. To reduce any form of uncertainty, I created a feature that shows users how these credits are calculated and how they can be accessed.

Conclusion

Biggest Learning: Design for Behaviour Change, Not Just Workflows

Even as a side project, the challenge wasn't designing screens; it was designing a system that convinced business owners who've managed money informally for years that tracking digitally was worth the effort. Every micro-interaction needed to provide immediate feedback that reinforced "this is making my business better."

Each feature isn't valuable in isolation. Value compounds when features feed into each other. Transaction tracking generates data → Invoicing creates credit opportunities → Credit usage drives more invoicing. Design the flywheel, not the features.

What I'd Change, if I had time and the resources:

1. Earlier testing of the payment flow

I designed the invoice payment experience based on assumptions about what would work. Reviewing the product with a couple of users, I discovered that users were confused by the split-settlement model (where payments partially repay credit). Should have prototyped this interaction much earlier, it's the core value prop.

2. More focus on "why", not just "how"

Initial designs showed users what to do ("Create an invoice") but not why it mattered to their business. Adding contextual education ("Professional invoices get paid 5 days faster on average") improved feature adoption. Should have led with value, not functionality.

3. Accounting for intermittent connectivity earlier

Halfway through the project, I realised many users would have unreliable mobile data. Redesigning for offline-first was painful. Should have made "works on 3G/intermittent connection" a core constraint from day one, not an afterthought.

Ledgerly

Categories

Fintech

Mobile App

Duration

2025-2026

Role

Product designer

Client

Side-Project

Overview

Helping Businesses Track Money, Send Invoices, and Access Credit

Designing a mobile-first fintech platform that helps small & medium businesses track money, send invoices, and access credit

While working on various fintech projects, I noticed a pattern: small business owners in Nigeria constantly struggled with cashflow visibility and access to working capital.

I started Ledgerly as a side project to explore: What if we could embed credit directly into the payment flow, turning invoices into instant working capital?

The Problem

Spreadsheets, WhatsApp, and Loan Sharks: Understanding How SMBs Actually Survive

Even as a side-project, I still had to put on my "UX research hat" to figure out what existing issues affected these SMBs. After speaking to some small business owners and close friends, I identified 3 critical issues:

Invisible cash flow: Most of them were used to tracking money in spreadsheets or paper notebooks. Most can't answer "How much did I make last month?" without spending hours reconstructing records.

Unprofessional payment collection: Sending bank details via WhatsApp feels informal and leads to errors, delayed payments, and lost revenue.

Credit access gap: Banks won't lend to informal businesses. When a large order comes in requiring upfront inventory purchases, business owners resort to high-interest "loan sharks" (20-30% monthly interest) or simply reject the opportunity.

From a product & business perspective, having an embedded finance opportunity was useful but challenging:

Lending to some of these SMBs without traditional credit histories requires alternative underwriting models.

Understanding the issues from the user and product perspective, I decided to craft a north-star problem statement that guided my design thinking from here on:

How do we design a product where each feature reinforces the others—where invoicing generates data for credit decisions, and credit access incentivizes more invoicing—creating a flywheel effect?

Opportunity

Progressive Value Delivery

Rather than building a feature-rich financial platform, I designed an interconnected product where each capability strengthens the other.

I structured the product as a value ladder where users naturally progress through increasingly valuable (and monetizable) features:

Solution

Key Design Decisions

Improving how users create invoices, recover funds and record expenses.

Users can create invoice templates to reduce the time spent on invoice creation. Invoices are sent to customers, who can pay automatically via an embedded payment link, and the user is notified when payment has been made.

To improve fund collection, the system periodically sends payment reminders to customers and enhances business fund collection.

Quick income/expense recording with OCR receipt scanning

Design for the 30-second use case

SMB owners rarely have 10 minutes to "do their books." The product had to work in stolen moments—between customers, during a commute, before bed. So, having a push notification that reminds users to record their daily financial activities would help users stay disciplined with their bookkeeping.

Intelligent defaults & smart suggestions over configuration

Based on user data and interaction with the app, the system auto-suggests possible descriptions of the user's expenses, and categories are based on past activities of the user. For instance, instead of asking users to categorise expenses manually, the system learns patterns and behaviour of the user, thereby personalising the experience of the user.

Contextual credit offers, not loan applications

Rather than making users "apply for a loan," credit appears contextually when they have unpaid invoices: "Customer hasn't paid yet? Get your money now—we'll collect when they pay." This reframing would change the mental model from "taking debt" to "accelerating my own money and helping my business to grow." This would reduce psychological resistance to credit.

Reducing the complexity of credit accessibility

One thing I discovered is that SMBs are quite sceptical when it comes to getting credit for their businesses, as they see it as a debt trap in the hands of regular loan sharks. To reduce any form of uncertainty, I created a feature that shows users how these credits are calculated and how they can be accessed.

Conclusion

Biggest Learning: Design for Behaviour Change, Not Just Workflows

Even as a side project, the challenge wasn't designing screens; it was designing a system that convinced business owners who've managed money informally for years that tracking digitally was worth the effort. Every micro-interaction needed to provide immediate feedback that reinforced "this is making my business better."

Each feature isn't valuable in isolation. Value compounds when features feed into each other. Transaction tracking generates data → Invoicing creates credit opportunities → Credit usage drives more invoicing. Design the flywheel, not the features.

What I'd Change, if I had time and the resources:

1. Earlier testing of the payment flow

I designed the invoice payment experience based on assumptions about what would work. Reviewing the product with a couple of users, I discovered that users were confused by the split-settlement model (where payments partially repay credit). Should have prototyped this interaction much earlier, it's the core value prop.

2. More focus on "why", not just "how"

Initial designs showed users what to do ("Create an invoice") but not why it mattered to their business. Adding contextual education ("Professional invoices get paid 5 days faster on average") improved feature adoption. Should have led with value, not functionality.

3. Accounting for intermittent connectivity earlier

Halfway through the project, I realised many users would have unreliable mobile data. Redesigning for offline-first was painful. Should have made "works on 3G/intermittent connection" a core constraint from day one, not an afterthought.